Institutional Insights: Goldman Sachs 'US Equity Markets Positioning & Key Levels'

CTAs have been major sellers, with an estimated $184bn of global equity selling over the past month, leaving the cohort currently short approximately $47bn.

Fundamental L/S managers underperformed less than the broader market, while systematic L/S strategies posted modest gains, driven primarily by alpha.

CTA Corner

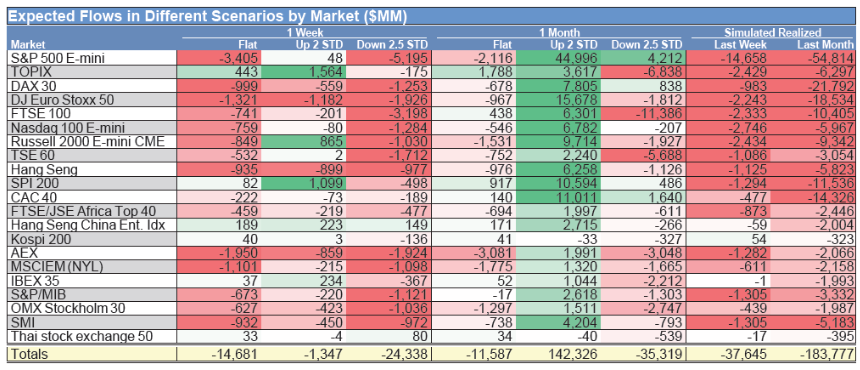

Looking ahead, CTA flow remains skewed defensive in the near term:

Next 1 week

Flat tape: -$15bn

Up tape: -$1bn

Down tape: -$24bn

Next 1 month

Flat tape: -$12bn

Up tape: +$142bn

Down tape: -$35bn

This reinforces a market structure in which upside can mechanically improve flows, while weakness still invites additional selling pressure.

SPX pivot levels

Short-term: 6756

Medium-term: 6745

Long-term: 6399

GS Prime Brokerage: Positioning Continues to De-Risk, But Gross Remains Elevated

Prime Brokerage data show another week of meaningful de-risking in net terms, even as gross exposure remains elevated. Overall book gross leverage rose to 313.7%, a five-year high, while net leverage fell to 71.3%, near the bottom decile of the past year. The decline in the overall long/short ratio to 1.588, a five-year low, reinforces the message: investors are reducing directional exposure, but not necessarily getting smaller across the board.

In fundamental long/short, the same pattern persists. Gross leverage eased only modestly, while net leverage fell more materially, suggesting managers continue to adjust exposure more through hedging and shorting than through broad balance-sheet reduction.

At the regional level, global equities were net sold for the sixth consecutive week, with this latest move representing the largest net selling since April 2025. Activity remained heavily skewed toward short sales, with gross flow driven by shorts over longs by 5.6 to 1. EM Asia saw especially aggressive selling—its fastest since April 2025—yet allocations to Asia remain near record highs on both a gross and net basis, underscoring how crowded the region still is despite recent liquidation.

In Europe, hedge funds sold equities for a sixth straight week, with the pressure driven entirely by macro-product shorts. Single stocks, by contrast, were modestly net bought. Short exposure in European macro products now stands at 11% of total regional exposure, a 10-year high, highlighting how aggressively investors are using index and macro instruments to hedge or express bearish views.

In the U.S., long/short gross leverage fell for a third straight week, but again, the more notable move was in net leverage, which posted its sharpest weekly decline since Liberation Day. Hedge funds sold U.S. equities for a sixth straight week and at the fastest pace since April 2025. Selling was particularly intense in U.S. TMT, which saw its largest percentage net selling since September 2024 and its third-largest sell week in the last five years. U.S. Industrials were also net sold for a fifth straight week.

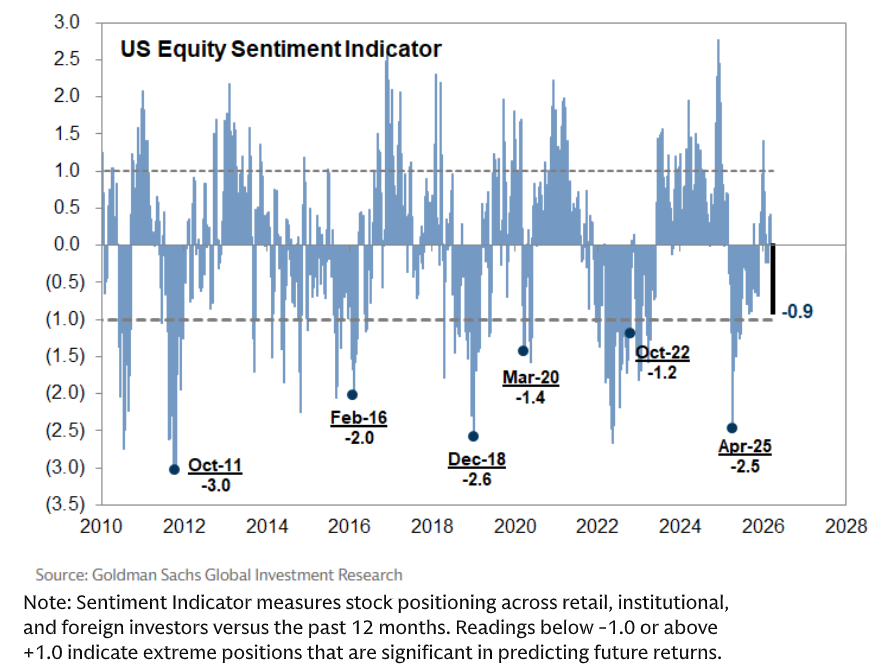

Sentiment indicators are now approaching levels that, historically, have tended to be more constructive for forward returns. Goldman’s U.S. Equity Sentiment Indicator fell to -0.9, nearing the -1.0 threshold that has historically been associated with above-average future performance, with stronger signals typically emerging below -1.5. At the same time, the U.S. Vol Panic Index remains deeply elevated at 9.2 / 10, with the market now in panic territory for 17 straight sessions—one of the longest such streaks in 15 years.

The takeaway is straightforward: net exposure is coming down quickly, but gross risk remains high, and the de-risking is still being expressed primarily through shorts and overlays rather than wholesale balance-sheet reduction. That combination keeps the market fragile, crowded, and vulnerable to sharp moves in either direction.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!