Institutional Insights: BofA Systematic Flow Monitor 16/0625

.jpeg)

Institutional Insights: BofA Systematic Flow Monitor 16/0625

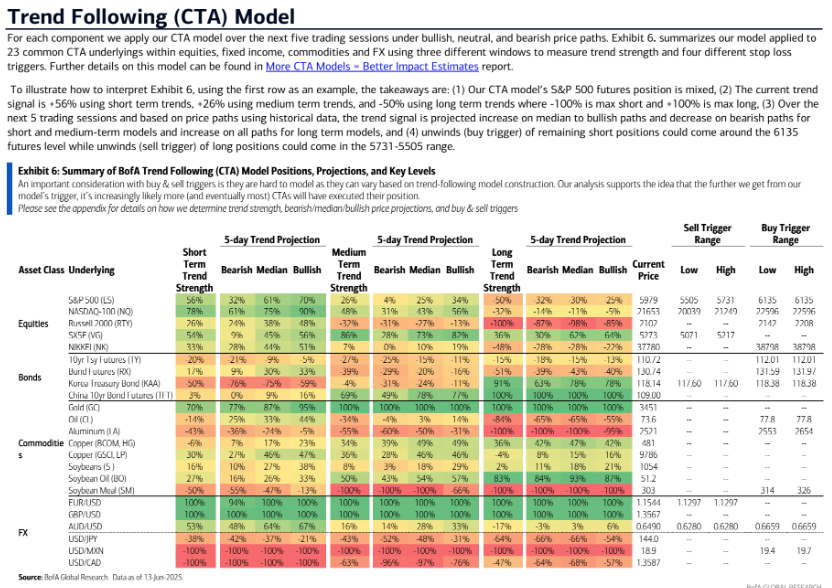

CTAs covered oil shorts, with some potentially starting to accumulate positions soon. This week, WTI crude oil saw its largest weekly increase since October 2022, with futures rising by 13%. The upward movement on Friday was largely influenced by heightened tensions in the Middle East due to Israel's strike on Iran. However, we believe that Wednesday's 4.9% gain was bolstered by trend followers closing short positions, as five out of the twelve trend-following models we track were stopped out on that day. Looking ahead to next week, the futures price trend may turn favorable for short- to medium-term models, which could lead some CTAs to take long positions. It's important to note that the accumulation of a CTA position generally occurs at a slower pace and has a less significant impact on the markets compared to the unwinding of a position.

In other commodities, CTAs are maintaining long positions in Gold and Soybean Oil, while being short on Aluminum and Soybean Meal. Trend followers might also increase their Soybean longs next week. They continue to hold sizable short positions in USD against EUR, GBP, and MXN, despite the US Dollar's decline this week, which coincided with rising geopolitical tensions on Friday. Our model shows that CTAs remain strongly in agreement and are close to their maximum long positions in EUR, GBP, and MXN versus USD. At this moment, their positions do not approach unwinding triggers and will only be at risk if the USD experiences a sharp rally. In contrast, JPY and CAD longs remain less stretched, and AUD positioning is mixed, with expected buying against USD in the upcoming week.

CTA positioning in equities and bonds varies by model. Long-term trend followers are still short on Russell 2000 and Nikkei 255 futures, while short- to medium-term trend followers are long on S&P 500, NASDAQ-100, and Nikkei 225 futures, with the EURO STOXX 50 long being the most consensus position. In fixed income, CTAs maintain short positions in 10Y US Treasury futures, but their positioning in other global bond futures is more diverse. Our model suggests that CTAs are likely to sell KTBs next week, irrespective of model parameters.

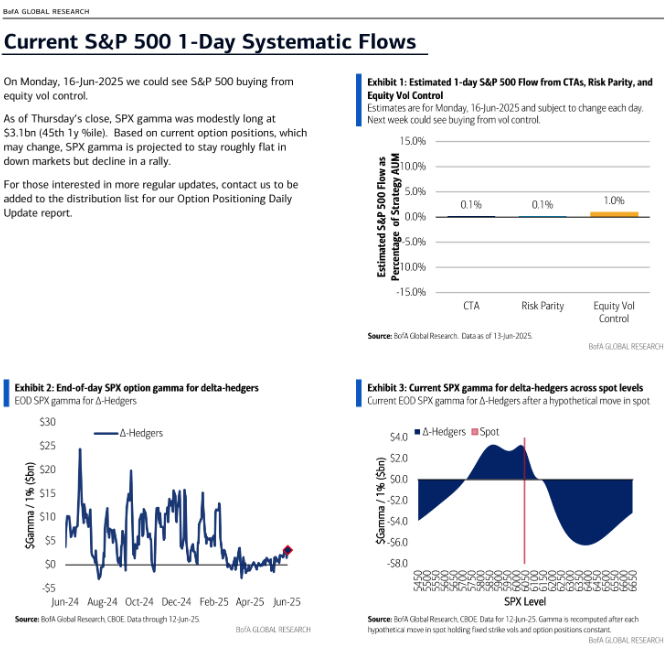

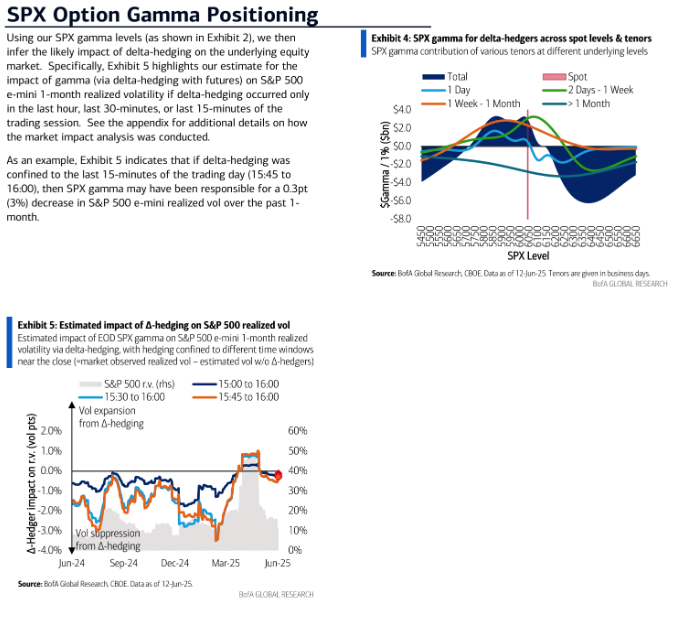

As of Thursday's close, SPX gamma was slightly long at $3.1 billion, sitting at the 45th percentile for the year. Based on current option positions—which may be subject to change—SPX gamma is expected to remain relatively stable in downward markets but could decline during a rally. For now, the reduction in equity realized volatility due to long SPX gamma is likely too minor to be particularly noticeable amid ongoing fundamental flows tied to a dynamic geopolitical environment. Positioning in the VIX ecosystem remains elevated, with the end-user VIX delta position in the 98th percentile for the year. For more details, refer to our daily option positioning report.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!